Ensuring Financial Stability And Resilience In Times Of Crises

Deposit insurance is a vital component to safeguarding financial stability, offering depositor protection and maintaining confidence. In commemoration of the Global Financial Crisis and the Asian Financial Crisis, we reflect on their impact on Malaysia’s financial system and how this led to the establishment of Perbadanan Insurans Deposit Malaysia (PIDM) and its contributions to financial system stability.

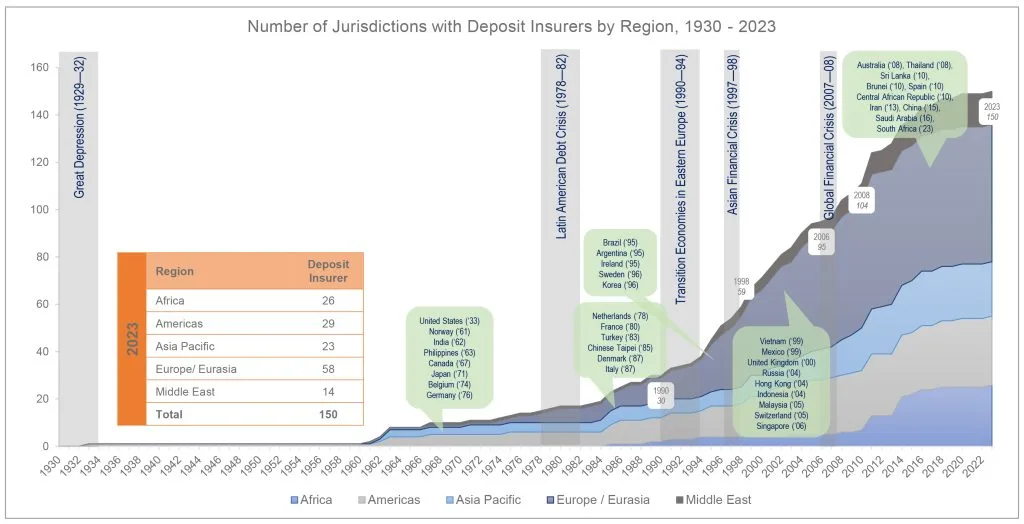

The inception of PIDM is a response to the aftermath of the 1997/98 Asian Financial Crisis. Malaysia’s experience in the crisis prompted it to fortify its financial system, leveraging adversity to cultivate resilience.

As part of the 10-year Financial Sector Masterplan unveiled by Bank Negara Malaysia (BNM), one of the pivotal measures was the establishment of a deposit insurance system to enhance public confidence in the country’s financial sector. Thus, PIDM emerged to fulfil its core objectives – safeguarding depositors, encouraging sound risk management among banks, and fairly distributing deposit insurance costs within the banking industry.

Not too long after PIDM’s inception in September 2005, the collapse of Lehman Brothers on 15 September 2008 spurred certain nations to quickly enact blanket guarantees to stem market-wide confidence crises. Malaysia mirrored this response on 16 October 2008, implementing the Government Deposit Guarantee (GDG) – with PIDM as its administrator – as a pre-emptive measure to quell potential cross-border capital flow contagion.

PIDM exited from the GDG in 2010, paving the way for its expanded role as a financial consumer protection authority. The exit was accompanied by the enhancement of coverage limits of the Deposit Insurance System (DIS) from RM60,000 to RM250,000 and the introduction of the Takaful and Insurance Benefits Protection System (TIPS) for takaful certificate and insurance policy owners.

PIDM Today – Empowering Resilience

PIDM wears two hats – a financial consumer protection authority and a resolution authority for member institutions. Its purview extends beyond mere guardianship of two protection systems; namely DIS and TIPS. For member institutions, achieving resolution readiness becomes a pivotal benchmark. This strategic initiative ensures PIDM’s ability to swiftly address financial distress among member banks.

Adapting To New Dynamics In A Changing Financial Landscape

In a rapidly changing financial landscape, Malaysia’s banking and financial system has grown in size, complexity, and interconnectedness with the economy. Lessons from the bank failures in the US earlier this year also highlight the speed at which regulators need to respond to mitigate a market-wide confidence crisis.

Hence, it becomes crucial for resolution authorities like PIDM, to have a comprehensive understanding of its member banks’ resolution readiness and identify early any potential impediments to resolvability. The phased roll-out of the resolution planning initiative in 2024 aims to minimise fallout in the event of a bank failure or financial crisis through effective and decisive resolution actions.

As part of planning, PIDM collaborates extensively with industry stakeholders to tailor these plans for individual member banks. Concurrently, it fosters collaboration with the likes of BNM, the Ministry of Finance, and foreign authorities to strengthen inter-agency plans and arrangements, thereby reinforcing the financial safety net.

In line with depositor expectations, PIDM partners with Payments Network Malaysia Sdn Bhd (PayNet) to facilitate seamless reimbursements in case of bank closure and liquidation. This seamless reimbursement approach mitigates potential disruptions during financial institution failures.

An Effective Just-In-Case Protection System

PIDM’s role is not to prevent failures; rather, our role as a just-in-case protection system is to ensure that failures can be resolved swiftly and effectively to preserve financial system stability.

After 18 years and with the learnings from past financial crises, PIDM continues to build upon its crisis readiness so that when we are called upon to deliver on our mandate, we can confidently say that we had the foresight to prepare for any eventuality.